The year is 2012. In a small village in Maharashtra’s Konkan, Laxmi, a 29-year-old single mother of two, dreams of building a life of dignity by earning a livelihood to sustain her family. She would visit the local post office every other week to claim her widow’s pension, but the relief she sought was unreliable. The meagre sum she received was barely enough for a month. Laxmi came from a background of artisans skilled in Sawantwadi crafts – the colourful and intricately carved wooden toys that once adorned markets across Maharashtra. She yearned to revive her family’s tradition by starting a small business. However, securing formal working capital was nearly impossible with no bank account.

In the early 2010s, India was still a long way from achieving financial inclusion. Only 35% of Indians had access to a formal bank account, with the data being even lower for women. Only 26% of women had access to a bank account. Women in states like Maharashtra, Rajasthan, and Uttar Pradesh were 50% less likely to have a bank account than men, highlighting the economic barriers they faced. This reality also shaped women’s entrepreneurship. According to the Sixth Economic Census (2013), only 13.76% of India’s enterprises were owned by women, reflecting systemic barriers such as low penetration of formal financial services, identification issues, and deeply rooted sociocultural norms that restrict women’s economic agency. With no formal credit access, women like Laxmi were forced to rely on informal moneylenders, borrowing at high interest rates under precarious terms, often leading to adverse outcomes and an insecure future. This was like a chain reaction, each unfortunate link pushing women backwards, towards invisibility and stripping them of opportunities to grow and be a part of India’s formal economy.

Fast forward to 2017, with a successful rollout of Aadhaar UID and Pradhan Mantri Jan Dhan Yojana, the late 2010s witnessed a seismic shift in women’s financial inclusion patterns. By 2017, 77% of adult women had a bank account, a sharp increase from just 26% in 2011. The gender gap in account ownership shrank from 22 percentage points in 2011 to virtually zero by 2021. For Laxmi, this transformation was life-changing. With a verifiable ID, Aadhaar, and her newly opened Jan Dhan account, Laxmi applied for a collateral-free loan under the Pradhan Mantri Mudra Yojana (PMMY), one of the safest and most accessible credit schemes for small business owners. With a streamlined e-KYC procedure and formal access to credit, she secured the working capital she could once only dream of. Laxmi set up her enterprise to revive traditional Sawantwadi crafts, rejuvenating the fading tradition of handcrafted wooden toys while stepping boldly into the formal economy.

Nearly 70% of Mudra loan beneficiaries are women entrepreneurs, representing millions of women across India, thousands of Laxmis who have leveraged India Stack to transform their lives, uplift their families, and spark new hopes for their communities through enterprise and resilience. With Aadhaar, UPI, and data protection, India Stack has been a key driver of inclusivity, not only financially, but also in terms of gender, bringing about social empowerment and boosting female entrepreneurship.

Successful Direct Benefit Transfers (DBT) of women-centric schemes like Pradhan Mantri Matru Vandana Yojana, Janani Suraksha Yojana, pension programs for widows and elderly women under NSAP, Jan Arogya Yojana, Balika Samriddhi Yojana, and other state government initiatives have built people’s trust in G2P paradigms and fostered a transparent and responsible environment. The national average for women’s participation in MGNREGA is 57.4%, with almost all major states reporting a female share of more than 33%.

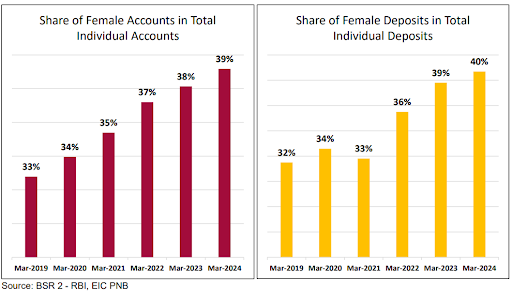

Over 55% of PMJDY account-holders are women beneficiaries. Today, women own nearly one-third of all bank accounts in India. Women’s per capita deposits have grown consistently over the past few years, cumulatively rising by ₹4,618 in FY23. Rural areas are the primary source of women’s deposits, with women holding 30% of the total rural deposits in FY23, compared to women’s share of only 16.5% in metropolitan areas. This gain is attributed to women-centric schemes for financial inclusion by Regional Rural Banks (RRB) and the government’s efforts towards women’s empowerment.

More women are entering the formal financial system and accumulating higher balances on average. By FY24, the all-India per capita deposit for women is estimated to have surpassed ₹45,000, up from ₹37,900 in FY19. SBI’s research highlights that SHGs (Self-Help Groups) have evolved into a “mass movement” in rural and semi-urban regions, enabling women to deposit regular savings. These small-ticket deposits collectively increase the total deposits held by women, even if the per capita figures remain low. Public sector banks have played a key role in supporting this trend, thereby formalizing and driving women’s savings in villages.

With savings leading to credit, when women maintain some funds, they become eligible for loans such as Self-Help Group credits or Mudra microenterprise loans. The share of women in credit to individuals increased in nine years from 18.3% in FY15 to 23% in FY23. Banks have disbursed nearly ₹10.3 trillion in incremental credit to 76 million new women borrowers over this period. This access to credit for agriculture, education, and trade empowers women economically, enabling them to generate income and accumulate assets, thereby transitioning them from passive savers to possessing better financial agency.

Launched in 2017 with the objective of skill development and fostering digital adoption by educating the rural population about the India Stack and digital technologies, the flagship initiative, PMGDISHA – Pradhan Mantri Grameen Digital Saksharta Abhiyan – has been instrumental in ushering digital literacy in rural India. As of March 2024, 6.39 crore individuals had completed the training, and 4.78 crore had received certifications. Covering a broad age group of 14-60, women accounted for over 54% of the trainees under the PMGDISHA program. Other initiatives, such as ‘Internet Saathi’ by Google India and Tata Trusts, helped train women in rural areas to use the internet, who went on to become trainers, spreading awareness to others in their communities. The initiative reached over 17 million women across 17,ooo villages by 2017, igniting the spark of inclusivity in digital India.

India Stack has played a pivotal role in advancing financial inclusion and narrowing the gender gap. As the country aspires to become a $30 trillion economy by its centenary in 2047, achieving this vision will require not just technological infrastructure but also equitable and accelerated participation of women in the formal economy. However, apart from thriving infrastructure development, a mindset shift is equally essential, breaking down the socio-cultural barriers that limit women’s agency. Many women, particularly those less educated or older, feel intimidated by banks and mobile technology, having traditionally relied on cash transactions and informal systems.

To foster deeper inclusion, there is a pressing need for expanded digital literacy initiatives, particularly those tailored for women and delivered in their vernacular languages. Gender-sensitive banking infrastructure, which includes a higher proportion of female banking correspondents, clerks, and digital instructors, can make financial spaces more approachable and supportive. Moreover, financial products must be simplified and localized to meet the needs of diverse customers. The dominance of English in banking forms, app interfaces, and service communication presents a significant barrier for many women. Designing user-friendly, vernacular financial tools and providing clear explanations can bridge this gap, enabling women to not only access but also confidently engage with the formal financial system.

Regular awareness campaigns on UPI, Aadhaar-enabled banking, DigiLocker, and consent-based data sharing are crucial to help women understand and effectively navigate India’s digital infrastructure. Equipping them with knowledge about data consent, OTP verification, and secure digital practices is crucial for informed usage and protecting them from fraud during financial transactions, digital identity use, or while availing loans.

The next frontier lies in designing infrastructure tools with empathy, communicating with clarity, and ensuring that every Indian woman, whether in a remote village or an urban corner, can assert her place in India’s digital revolution with competence and integrity.

The views and opinions expressed here belong solely to the author and do not reflect the views of BlueKraft Digital Foundation.